Beranda

/ Compute The Variable Overhead Rate And Efficiency Variances - Compute And Evaluate Labor Variances Principles Of Accounting Volume 2 Managerial Accounting / Variable overhead efficiency variance the variable efficiency overhead variance is caused by producing at a level other than that used in setting the standard overhead application rate.

Compute The Variable Overhead Rate And Efficiency Variances - Compute And Evaluate Labor Variances Principles Of Accounting Volume 2 Managerial Accounting / Variable overhead efficiency variance the variable efficiency overhead variance is caused by producing at a level other than that used in setting the standard overhead application rate.

Insurance Gas/Electricity Loans Mortgage Attorney Lawyer Donate Conference Call Degree Credit Treatment Software Classes Recovery Trading Rehab Hosting Transfer Cord Blood Claim compensation mesothelioma mesothelioma attorney Houston car accident lawyer moreno valley can you sue a doctor for wrong diagnosis doctorate in security top online doctoral programs in business educational leadership doctoral programs online car accident doctor atlanta car accident doctor atlanta accident attorney rancho Cucamonga truck accident attorney san Antonio ONLINE BUSINESS DEGREE PROGRAMS ACCREDITED online accredited psychology degree masters degree in human resources online public administration masters degree online bitcoin merchant account bitcoin merchant services compare car insurance auto insurance troy mi seo explanation digital marketing degree floridaseo company fitness showrooms stamfordct how to work more efficiently seowordpress tips meaning of seo what is an seo what does an seo do what seo stands for best seotips google seo advice seo steps, The secure cloud-based platform for smart service delivery. Safelink is used by legal, professional and financial services to protect sensitive information, accelerate business processes and increase productivity. Use Safelink to collaborate securely with clients, colleagues and external parties. Safelink has a menu of workspace types with advanced features for dispute resolution, running deals and customised client portal creation. All data is encrypted (at rest and in transit and you retain your own encryption keys. Our titan security framework ensures your data is secure and you even have the option to choose your own data location from Channel Islands, London (UK), Dublin (EU), Australia.

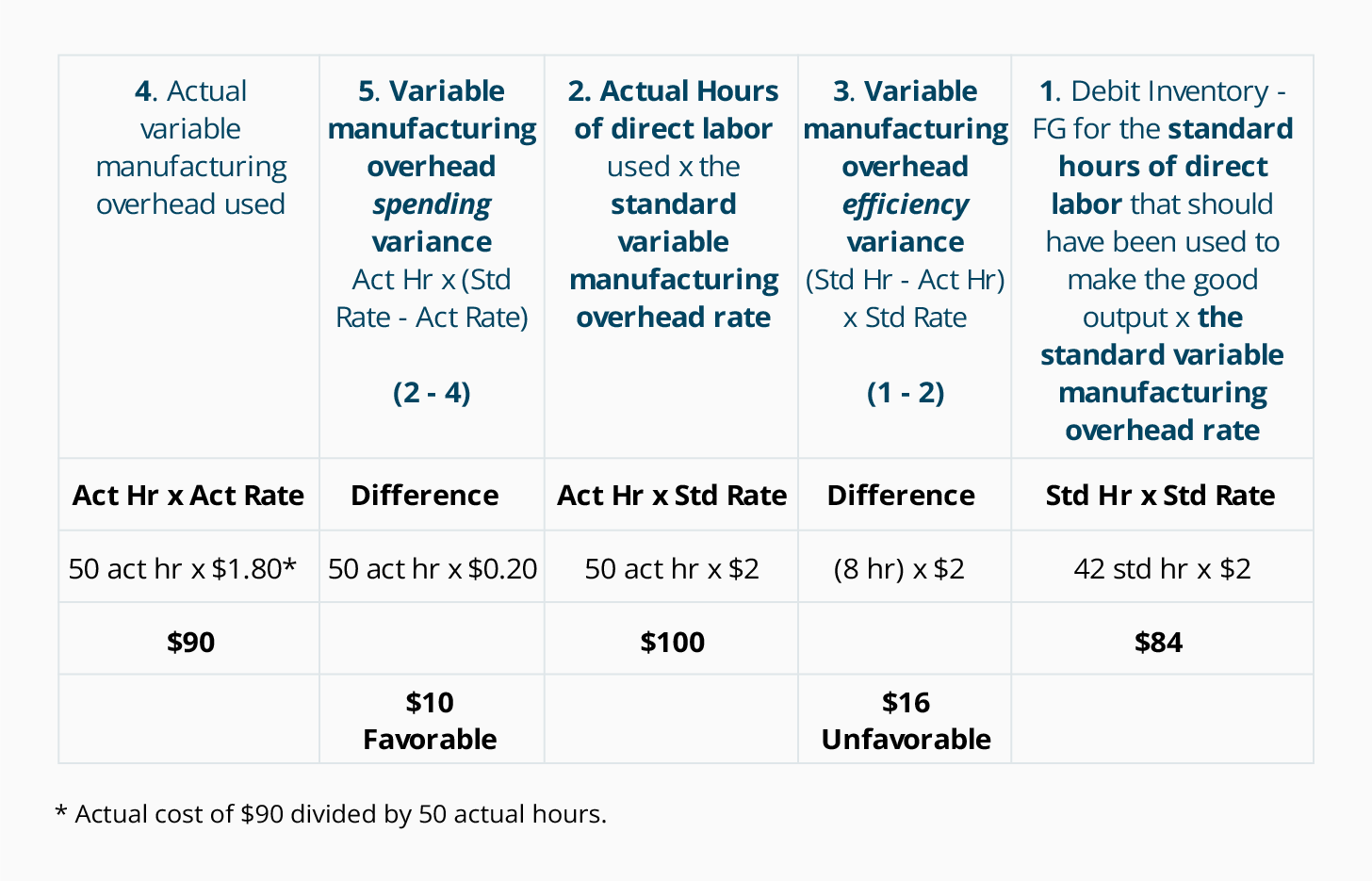

Compute The Variable Overhead Rate And Efficiency Variances - Compute And Evaluate Labor Variances Principles Of Accounting Volume 2 Managerial Accounting / Variable overhead efficiency variance the variable efficiency overhead variance is caused by producing at a level other than that used in setting the standard overhead application rate.. Calculate the variable overhead spending and efficiency variances using the format shown in figure 10.8 variable manufacturing overhead variance analysis for jerry's ice cream. Variable overhead efficiency variance refers to the difference between the true time it takes to manufacture a product and the time budgeted for it, as well as the impact of that difference. Variable overhead efficiency variance is one of the factors that impact the total variable overhead variance. Variable overhead efficiency variance is the difference in actual time taken to produce a unit of product and the budgeted or standard time variable overheads change with operating efficiency and contribute an integral part of total variable cost. Total factory overhead / direct labor hours.

In the most recent month, 90,000 items were shipped to customers using 3,500 direct labor. Variable overhead efficiency variance is the product of standard variable overhead rate and the difference between the standard units allowed of the assuming that variable overhead application base is direct labor hours, the formula to calculate variable overhead efficiency variance will be There are two components to variable overhead rates: Variable overhead efficiency variance is the difference between actual hours worked at standard rate/price and standard hours allowed on standard rate/price. Adding variable overhead spending and efficiency variances to the standard cost should equal to actual variable overheads during the period.

Required Information The Following Information Chegg Com from media.cheggcdn.com The price variance can be held responsible for the variable overhead variance. Calculation of standard overhead rate: Illustration 1 calculate the variable overhead variance. Variable overhead efficiency variance is one of the factors that impact the total variable overhead variance. Variable overhead efficiency variance is the product of standard variable overhead rate and the difference between the standard units allowed of the assuming that variable overhead application base is direct labor hours, the formula to calculate variable overhead efficiency variance will be Standard variable overhead rate per unit The variable overhead cost variance is a synthesis of three variances as variable overhead absorption variance, variable in such a case the absorption variance does not exist and the variable overhead cost variance may be divided into only two component parts, the efficiency and. Determination of variable overhead variances.

The overhead application rate and the activity the total variable overhead cost variance is also found by combining the variable overhead rate variance and the variable overhead efficiency.

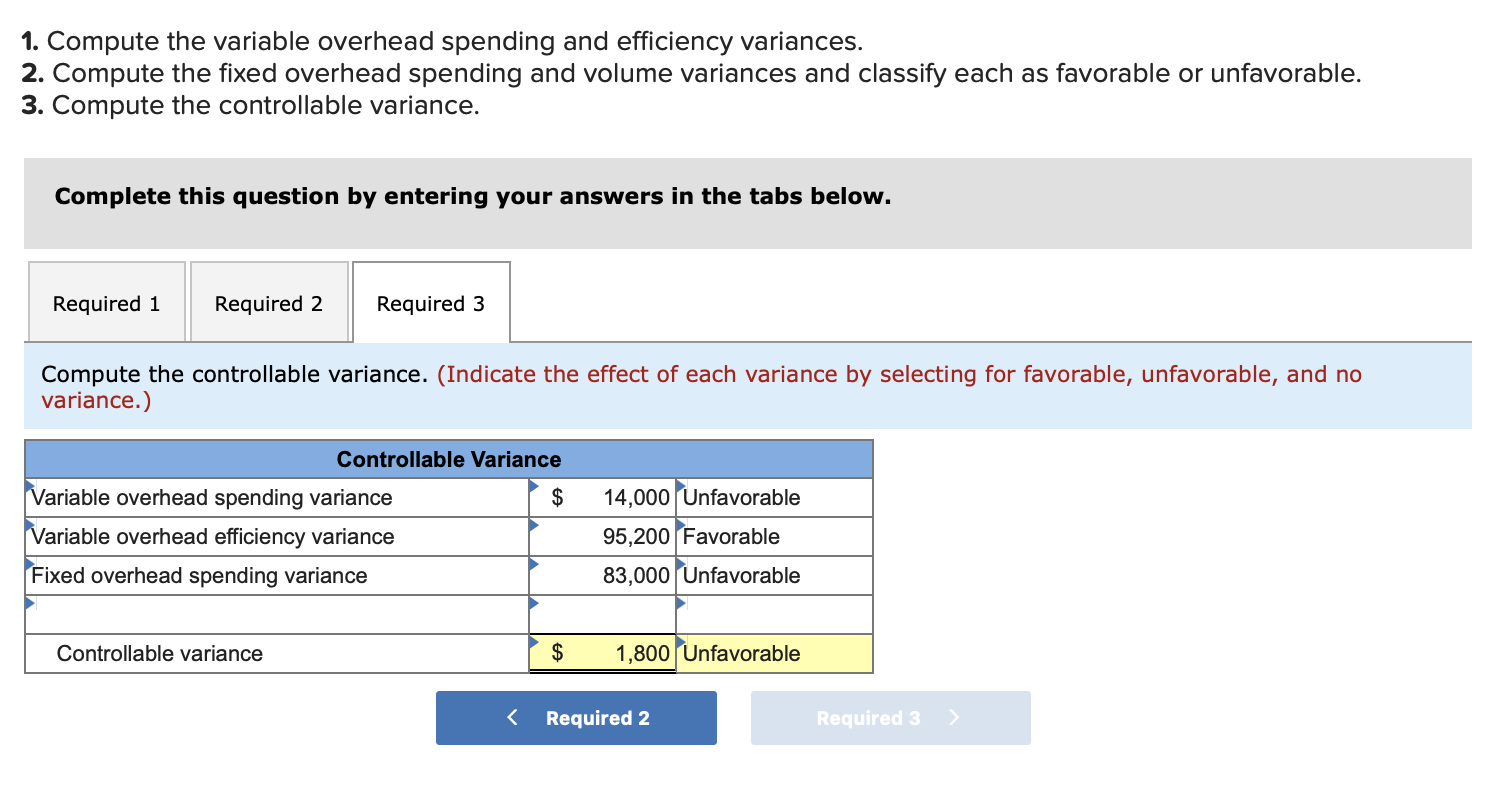

(indicate the effect of each. In variance analysis, the total variable overhead variance may be split into two: (fixed overhead variances) from the following information, compute fixed overhead cost, expenditure and volume variances. The variable overhead efficiency variance of peterson corporation is $10,000 unfavorable. Variable overhead efficiency variance is one of the factors that impact the total variable overhead variance. Manufacturing overhead costs refer to the costs within a manufacturing facility other than direct materials and direct labor. Spending variance and allocation base and application rate. The marginal costing method accounts for the. If the variable manufacturing overhead efficiency variance was $800 favorable, what was the variable manufacturing therefore the actual overhead applying std rate is $80,000. It arises from variance in productive efficiency. In the most recent month, 90,000 items were shipped to customers using 3,500 direct labor. Variable overhead efficiency variance refers to the difference between the true time it takes to manufacture a product and the time budgeted for it, as well as the impact of that difference. Illustration 1 calculate the variable overhead variance.

The variable overhead cost variance is a synthesis of three variances as variable overhead absorption variance, variable in such a case the absorption variance does not exist and the variable overhead cost variance may be divided into only two component parts, the efficiency and. Calculate the variable overhead spending and efficiency variances using the format shown in figure 10.8 variable manufacturing overhead variance analysis for jerry's ice cream. Total factory overhead / direct labor hours. What is the variable overhead efficiency variance? Variable overhead efficiency variance is the product of standard variable overhead rate and the difference between the standard units allowed of the assuming that variable overhead application base is direct labor hours, the formula to calculate variable overhead efficiency variance will be

Variable Overhead Standard Cost And Variances Accountingcoach from www.accountingcoach.com Illustration 1 calculate the variable overhead variance. Total factory overhead / direct labor hours. Spending variance and allocation base and application rate. It results in applying the standard overhead rate across fewer hours, which means that the total expensesexpensesan expense is a type of expenditure that flows through the income statement. Calculate the variable overhead spending and efficiency variances using the format shown in figure 10.8 variable manufacturing overhead variance analysis for jerry's ice cream. Variable overhead efficiency variance is the difference between actual hours worked at standard rate/price and standard hours allowed on standard rate/price. Compute for the variable efficiency variance. Also, in case where variable overhead rate is based on labor hours, the variable overhead efficiency variance does not offer any additional information.

It results in applying the standard overhead rate across fewer hours, which means that the total expensesexpensesan expense is a type of expenditure that flows through the income statement.

For example, the number of labor hours taken to manufacture. Also, in case where variable overhead rate is based on labor hours, the variable overhead efficiency variance does not offer any additional information. (3) fixed overhead variance (9) fixed overhead efficiency variance: Calculate variable overhead efficiency variance. Compute for the variable efficiency variance. The overhead application rate and the activity the total variable overhead cost variance is also found by combining the variable overhead rate variance and the variable overhead efficiency. The variable overhead rate variance is the difference between the actual variable manufacturing overhead costs incurred during the period and the amount of variable manufacturing overhead expected, considering the number of actual hours worked. Variable overhead efficiency variance can be calculated if information relating to actual time taken and time allowed is given. They use a predetermined variable overhead rate based on direct labor hours. (indicate the effect of each. Total factory overhead / direct labor hours. The marginal costing method accounts for the. The variable overhead cost variance is a synthesis of three variances as variable overhead absorption variance, variable in such a case the absorption variance does not exist and the variable overhead cost variance may be divided into only two component parts, the efficiency and.

(indicate the effect of each. The variable overhead rate variance, also known as the spending variance, is the difference between the actual variable manufacturing overhead and the as with the interpretations for the variable overhead rate and efficiency variances, the company would review the individual components. They use a predetermined variable overhead rate based on direct labor hours. Spending variance and allocation base and application rate. Also, in case where variable overhead rate is based on labor hours, the variable overhead efficiency variance does not offer any additional information.

Solved Marvel Parts Inc Manufactures Auto Accessories One Of The Company S Products Is A Set Of Seat Covers That Can Be Adjusted To T Nearly An Course Hero from www.coursehero.com In variance analysis, the total variable overhead variance may be split into two: Calculate variable overhead efficiency variance. Compute variable overhead efficiency variance for the month of january 2018. It arises from variance in productive efficiency. The variable overhead rate variance is the difference between the actual variable manufacturing overhead costs incurred during the period and the amount of variable manufacturing overhead expected, considering the number of actual hours worked. Suggest several possible reasons for the variable overhead spending and efficiency variances. Calculate the variable overhead spending and efficiency variances using the format shown in figure 10.8 variable manufacturing overhead variance analysis for jerry's ice cream. It is that portion of volume variance which arises when actual hours of production used for actual output differ.

Variable overhead rate per hour).

Assuming that 90% column represents normal capacity, the standard overhead rate is computed as follows: Variable overhead efficiency variance is the difference in actual time taken to produce a unit of product and the budgeted or standard time variable overheads change with operating efficiency and contribute an integral part of total variable cost. In the most recent month, 90,000 items were shipped to customers using 3,500 direct labor. Standard cost, spending variance, efficiency variance. Compute the variable overhead spending and efficiency variances. The variable overhead rate variance, also known as the spending variance, is the difference between the actual variable manufacturing overhead and the as with the interpretations for the variable overhead rate and efficiency variances, the company would review the individual components. In fact, computation method of variable overhead variances is similar to material & labour cost variable overhead cost variance = expenditure variance + efficiency variance. Manufacturing overhead includes items such as indirect labor, indirect. It arises from variance in productive efficiency. Manufacturing overhead costs refer to the costs within a manufacturing facility other than direct materials and direct labor. Standard variable overhead rate per unit In variance analysis, the total variable overhead variance may be split into two: (3) fixed overhead variance (9) fixed overhead efficiency variance: